A global market growing at 8.69% annually. Seven competing technologies. Eight cuisine traditions with different needs. One very consequential question: what happens when the world’s 3.5 billion LPG users need an alternative?

I did not expect a market research project to make me question how I cook.

When I started building Navadhi’s Global LPG Alternatives Market report, I assumed it would be a clean energy transition story – the kind where solar and induction are obviously better and the only question is how fast adoption happens. What I found instead was considerably more complicated, more culturally interesting, and in certain segments more commercially urgent than I anticipated.

The urgency is partly the Iran War. On February 28, 2026, US-Israel strikes on Iran effectively closed the Strait of Hormuz – through which approximately 35% of globally traded LPG transits. LPG prices surged 22–35% in 19 days. In India, Indonesia, and the Philippines, physical cylinder shortages appeared before price signals did. This is not a commodity price event. It is a physical supply architecture failure. The global food system is more dependent on a 33-kilometre-wide waterway than most people – including most policymakers – realised.

But the Iran War is an accelerant, not the cause. The cause is structural: LPG’s cost and availability model was already under pressure from economics (induction is 37% cheaper than LPG in India at 2025 prices), from regulation (EU gas appliance bans, India’s PNG expansion mandate), from technology (solar cooker costs collapsing along a trajectory that mirrors solar panels), and from the demographic reality that the world’s fastest-growing LPG-dependent populations – in Sub-Saharan Africa and South and Southeast Asia – are also the populations for whom LPG price volatility is most catastrophically disruptive.

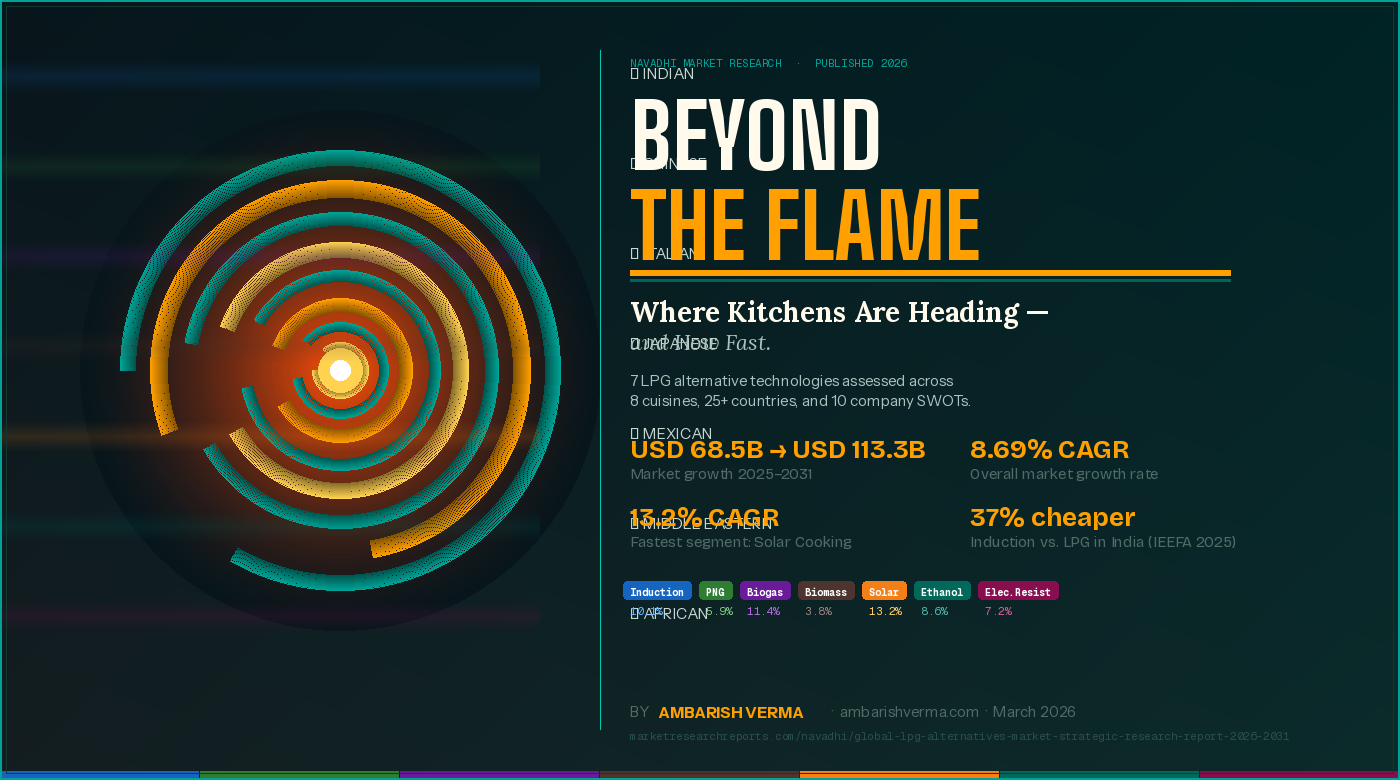

What We Found: USD 68.5 Billion LPG Alternatives Market in 2025 Growing to USD 113.3 Billion by 2031

The global LPG Alternatives market – defined as all cooking fuel solutions and cooking equipment specifically designed to replace LPG in households, commercial kitchens, and institutional food service – was worth USD 68.5 billion in 2025. Our forecast puts it at USD 113.3 billion by 2031, a CAGR of 8.69%. That growth rate places it among the fastest-growing market segments in the global energy and appliance landscape.

The growth is not evenly distributed. The fastest-growing segment is Solar Cooking (13.2% CAGR) – driven by the cost collapse of parabolic and evacuated-tube solar cookers as Chinese manufacturing applies the same learning curve model that reduced solar panel costs 90% over a decade. The largest segment is Electric Induction Cooking (growing at 10.1% CAGR by 2031) – driven by a combination of LPG price economics, regulatory mandates in Europe, and the progressive resolution of the culinary technique barriers that previously limited adoption in Asian markets.

The most intellectually interesting segment is Biogas and Biomethane (11.4% CAGR), because it is simultaneously a rural household cooking solution (family biogas digesters in India and Kenya converting agricultural waste to cooking fuel) and an urban infrastructure play (EU biomethane grid injection reaching 35 bcm by 2030). When biomethane is injected into the PNG network, piped gas cooking becomes a renewable fuel without requiring consumers to change any appliance. That convergence between the PNG and biogas segments is the single most strategically significant infrastructure development in the market for 2026–2031.

The Finding I Had Not Anticipated: Cuisine Determines Technology

The section of this report I am most proud of – and the one that is most unlike anything published on clean cooking markets – is the cuisine-by-cuisine LPG alternative suitability analysis.

Standard market research on LPG alternatives treats cooking as a generic activity. Apply heat. Food is prepared. LPG alternative is used. The reality is that different cuisine traditions have fundamentally different heat requirements, different flame-interaction techniques, and different culinary cultural relationships with fire – and these differences determine which LPG alternative is commercially viable for which population.

Consider the contrast between Japanese and Chinese cuisine. Japanese cooking – ramen broth simmering, sukiyaki tabletop cooking, tempura deep frying – is actually quite well served by electric induction. Precise, stable temperature control is a virtue in Japanese technique. Japan is already at 82% induction adoption in new kitchen builds, and the transition is essentially complete in urban residential markets.

Chinese cooking is the opposite problem. Wok hei – the characteristic ‘breath of the wok’ that professional Chinese chefs describe as the essential quality of properly prepared stir-fry – requires instantaneous contact with flames burning at temperatures of 500°C+ with commercial gas burners rated at 15,000–35,000 BTU/hour. Standard household induction cooktops deliver approximately 12,000 BTU equivalent at maximum power. The gap is real, measurable, and matters intensely to the 1.5 billion people in China and diaspora communities for whom wok hei is not an optional quality but a definition of what food should taste like.

| Silicon carbide (SiC) power transistors are enabling a new generation of commercial induction units operating at 12–20kW – approaching the BTU output of professional Chinese gas wok burners. COOKTEK and Ace Induction have demonstrated working prototypes. When this technology reaches USD 400–800 commercial price points (currently USD 2,000+), approximately 500,000 commercial Chinese kitchens in China alone will transition to induction. We project this around 2027–2028. |

Indian cuisine presents a different, more immediately solvable problem. The critical technique is tadka – heating ghee or oil to 280–300°C and adding spices that must bloom in seconds. High-power induction achieves this. The real barrier is cultural: the visual cue of oil shimmering over a gas flame is embedded in the cooking practice of hundreds of millions of Indian households. Induction removes the visual feedback loop. This is a behaviour change challenge more than a technical one – and behaviour change challenges respond to economic incentives. At 37% lower operating cost than LPG, Indian households are finding the behaviour change increasingly worth making.

What Drives This Market – and What Holds It Back

From the full drivers and inhibitors analysis in the report, these are the four dynamics that I think are most consequential for the 2026–2031 period.

- Economics have crossed the tipping point Induction is cheaper than LPG. Not marginally cheaper – materially cheaper at a level that changes procurement decisions. In India (37%), in Indonesia (growing cost differential), and in commercial kitchens globally (where Scope 3 carbon accounting makes the operating cost comparison even more favourable to electric). This economic crossover is the most important driver and the least reversible one – manufacturing learning curves do not reverse.

- The Iran War has permanently elevated supply security Governments that experienced LPG supply chain failure in March 2026 will implement strategic reserves, energy diversification mandates, and LPG alternatives infrastructure investments that will remain in place even after Gulf supply normalises. The policy architecture being built in the crisis window is durable.

- Biomethane grid injection solves the PNG compatibility problem The biggest objection to PNG as an LPG alternative – it is still a fossil fuel – is being resolved by EU biomethane mandates that will make city gas networks increasingly renewable. This is a 2027–2030 story, but its commercial implications for the PNG segment are significant.

- Sub-Saharan Africa is approaching a scale inflection The convergence of committed capital (USD 2.5B from AfDB and World Bank clean cooking funds), PAYG financing infrastructure (M-Pesa, MTN Mobile Money), and a genuinely competitive technology landscape (PAYG induction, solar, ethanol) means that Africa’s clean cooking transition is no longer a development aspiration – it is a commercial event with a quantifiable timeline.

The most significant inhibitor is the post-conflict LPG price normalisation risk – when Gulf supply returns, LPG’s cost competitiveness with alternatives will partially recover, reducing adoption urgency in price-sensitive markets. The structural solution is to lock in policy mandates and commercial contracts during the crisis window, before the economic urgency reduces. That is exactly what the governments, commercial kitchen operators, and energy companies that understand this market are doing right now.

A Note on How This Research Changed My Thinking

The aspect of this research that most changed how I think about energy transition is the cuisine section. Not because of what it reveals about LPG alternatives specifically, but because of what it reveals about how market research on energy transition usually fails.

Energy transition analysis almost always treats demand as generic – energy in, activity out. It almost never engages with the specific cultural practices that determine how energy is actually used, by whom, and with what emotional and practical attachment. The result is forecast models that are technically correct and commercially misleading at the same time: they accurately capture aggregate energy flows while missing the specific friction points that determine whether individual households and businesses actually make the switch.

The wok hei problem is not an engineering problem. It is an anthropology problem that has an engineering solution on a specific timeline. Understanding that distinction changes how you forecast adoption in Chinese cooking markets by several years. The chapati puffing problem in Indian cooking is a different kind of problem – it is a sensory feedback problem that can be addressed through consumer education and design, not through raw BTU output. These distinctions matter for companies deciding where to invest in product development, and for governments deciding which LPG alternatives to incentivise for which populations.

The global LPG Alternatives market is not one market. It is eight markets shaped by eight different culinary traditions, each with their own technology fit, their own adoption timeline, and their own commercial opportunity. The aggregate CAGR of 8.69% is the summary statistic. The cuisine analysis is the actual commercial intelligence.

Global LPG Alternatives Market Strategic Research Report 2026-2031 by Navadhi Market Research

About the Report

Navadhi’s Global LPG Alternatives Market Strategic Research Report 2026–2031 covers: 7 technology segment forecasts with year-by-year values through 2031; cuisine-by-cuisine suitability assessment for 8 global food traditions; 23-country LPG dependency analysis; Porter’s Five Forces, PESTLE, and full market SWOT; 10 company profiles with full SWOT analyses; and key future trends. 98 pages. USD 1,950 Single User. Published March 2026.

📄 Full Report: marketresearchreports.com/navadhi/global-lpg-alternatives-market-strategic-research-report-2026-2031

Leave a Reply